OBBB Premium Subsidy Increases in Basic, Optional, and Enterprise Units

- ARPC NDSU

- Jul 16, 2025

- 5 min read

Updated: Jul 26, 2025

by Dylan Turner and Shawn Arita

Introduction

The One Big Beautiful Bill Act (OBBB), signed into law on July 4, 2025, represents the most significant restructuring of federal crop insurance premium subsidies in the past two decades. While much attention has focused on the legislation's commodity program improvements and tax provisions, the crop insurance changes embedded within the OBBB mark a notable departure from the subsidy rates that have been in place since the early 2000s.

The legislation provides the first meaningful adjustment to Basic and Optional Unit subsidy rates since 2000, raising them by three to five percentage points across coverage levels. Although no changes to Enterprise Unit subsidy rates are explicitly stipulated in the OBBB, the Federal Crop Insurance Act was amended in the 2008 Farm Bill to mandate that Enterprise Unit subsidies provide "the same dollar amount of premium subsidy per acre that would otherwise have been paid by the Corporation under paragraph (2) if the policyholder had purchased a basic or optional unit for the crop for the crop year". In response to this, starting with the 2009 crop year, subsidy rates for enterprise units were raised to 80% for most coverage levels (the maximum allowable subsidy rate specified in the FCIA) with the remaining coverage levels rising to between 53% and 77% (depicted in table 1).

The process used to calculate these subsidy rate increases is described by RMA here, which in essence involves calculating the premium rate for each policyholder’s non-purchased unit structure and comparing the resulting difference in the premium paid per acre. These differences were then used to construct a weighted average discount for enterprise units. This requirement means that the OBBB's explicit subsidy increases for Basic and Optional Units could ultimately require corresponding adjustments to Enterprise Unit subsidy rates, potentially creating a cascade effect that extends beyond the legislation's explicitly stated provisions.

Figure 1. Crop Insurance Subsidy Rates by Coverage and Unit Structure

Note: Subsidy rates in figure 1 are empirically calculated using RMA’s summary of business by type, practice, and unit structure. Minor variations in year-to-year subsidy rates depicted are due to additional premium support payments that vary by year such as additional premium support for beginning farmers.

Increases in Premium Support Specified for Basic and Optional Units, Enterprise Units to be Determined

It is unclear if the subsidy rate increases in the OBBB to basic and optional units will ultimately prompt an adjustment to enterprise unit subsidy rates given that the FCIA states that this parity be maintained to “the maximum extent practicable”. As a cursory estimate of what this type of adjustment may look like, the ratio of acreage-weighted paid subsidies per acre between enterprise and basic units were calculated for the 2023 crop year using RMA’s summary of business. These ratios were then used to derive the approximate subsidy rate increase that would be required to maintain per acre subsidy equivalence under the OBBB.

The results of this exercise are reported in table 1. Coverage levels that were previously set at an 80% subsidy rate are already at the maximum allowable rate and are not expected to change. Under a readjustment, the EU subsidy rate at the 75% coverage level is expected to also rise to 80% with the remaining coverage levels rising to 72% and 57% respectively.

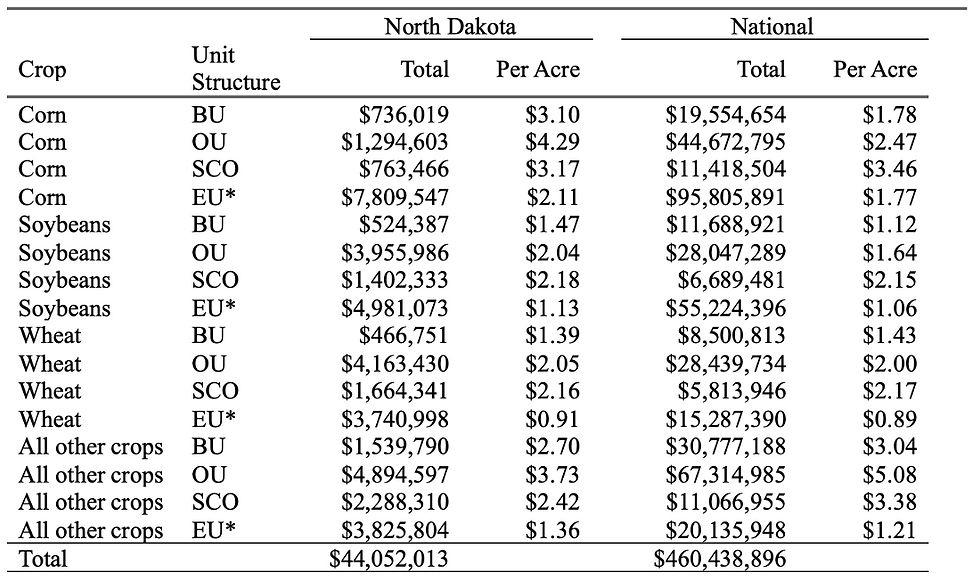

Table 1: Premium Support on Farm-Level Crop Insurance Programs: Current vs OBBB

Note. *Enterprise/Whole Farm unit premium support rates estimated using a weighted average approach described by https://legacy.rma.usda.gov/news/2008/11/1104wholefarm.html.

It is worth stressing that the process used here to estimate the increase in EU subsidy rates is not a perfect replica of what was used in 2008/09. The estimates here are based on the data in the public RMA summary of business and the observed differences in current premium support per acre. This means there is an implicit assumption in this analysis that there is no selection bias in who purchases basic/optional versus enterprise units[1]. Operating under the assumption that the increases estimated here are rough approximations of what an actual subsidy rate adjustment would look like suggests potentially much higher levels of premium support under the OBBB than what the explicitly defined increases to BU/OU would suggest. Estimates of the additional subsidy benefits of the OBBB (beyond what is currently provided) are reported in Table 2. These estimates are based on 2024 participation data, meaning constant crop insurance purchasing behavior is assumed (i.e. the new subsidy rates do not prompt producers to change their policy[2]). The increased benefits stemming from raising the subsidy rate on the supplemental coverage option (SCO) from 65% to 80% are also included. SCO in particular received several other modifications including raising the coverage level from 85% to 90% and allowing simultaneous participation in ARC-CO. Ignoring the behavioral response to higher coverage levels and these new flexibilities may thus understate future subsidy benefits of SCO.

Premium Support Benefits for North Dakota and Farmers Nationwide

Overall, the additional subsidy benefits stemming from the explicitly defined subsidy changes in the OBBB (BU, OU, and SCO) amount to about $24 million annually for North Dakota farmers and $274 million nationally. The estimated increases in EU subsidy rates amount to an additional $20 million for North Dakota and $186 million nationally. In total, this means the total premium support provided by the OBBB could increase by as much as $44 million per year for North Dakota and up to $460 million per year for the entire U.S, equivalent to an increase in paid subsidies of about 5.2% (ND) and 4.8% (U.S.) relative to the 2024 crop year[3].

Table 2: Additional crop insurance subsidy benefits under OBBB

Note. *Enterprise/Whole Farm unit premium support rates estimated using a weighted average approach described by https://legacy.rma.usda.gov/news/2008/11/1104wholefarm.html.

Conclusions

The OBBB's premium subsidy provisions mark the most substantial update to federal crop insurance support in a generation. After more than two decades of largely fixed subsidy rates, the legislation delivers meaningful increases for Basic and Optional Units and, by statutory design, may trigger corresponding upward adjustments for Enterprise Units. The analysis demonstrates that these changes translate into significant increases in support for producers nationwide—$44 million annually for North Dakota and over $460 million nationally, representing increases of approximately 5% over 2024 levels. Enhanced premium subsidies arrive as farmers navigate economic pressures that have reduced net farm income and heightened demand for comprehensive risk management tools. For producers, particularly in states like North Dakota where crop insurance protects millions of acres of diverse commodities, these subsidy improvements represent a meaningful strengthening of the agricultural safety net.

Related Research and Policy Analysis by ARPC Economists:

Tsiboe, F., & Turner, D. (2023). The crop insurance demand response to premium subsidies: Evidence from U.S. Agriculture. Food Policy, 119, 102505. https://doi.org/10.1016/j.foodpol.2023.102505

Tsiboe, F., Turner, D., & Yu, J. (2025). Utilizing large-scale insurance data sets to calibrate sub-county level crop yields. Journal of Risk and Insurance, 92(1), 139–165. https://doi.org/10.1111/jori.12494

___________

Notes

[1] Historically, there were notably different yield distributions between basic/optional and enterprise unit structures (Figure 5, Tsiboe et al., 2025) which would influence the premium paid. However, shortly after the EU subsidy rate was raised in 2009, this difference seems to have been mitigated with yield distributions being approximately the same for all unit structures since 2013.

[2] Past research suggests the participation response to changes in out of pocket cost of crop insurance is relatively small (Tsiboe & Turner, 2023)

[3] Based on RMA’s Summary of Business by Type, Practice, and Unit structure as of July 7th 2025.

Comments