Routine Pricing Adjustments Help Keep Crop Insurance Costs in Check

- ARPC NDSU

- Feb 17

- 4 min read

By Francis Tsiboe and Evelyn Osei

Government-subsidized agricultural insurance plays a major role in helping farmers manage weather, yield, and price risks while supporting stable food production and rural economies. In the United States, farmers often combine their own risk management strategies with coverage from the U.S. Federal Crop Insurance Program, one of the largest public-private insurance programs in the world. While the program delivers important benefits, it also represents a significant and growing cost to taxpayers, placing it at the center of ongoing policy debates about efficiency and fiscal responsibility.

From 2001 through 2023, the federal government covered about 61 percent of farmers’ crop insurance premiums and provided additional payments to private insurance companies to deliver the program na- tionwide. Over that period, the program insured hundreds of millions of acres each year and protected more than $200 billion in farm production annually. On average, total taxpayer costs exceeded $9 billion per year and grew rapidly over time. Because of this scale, even small improvements in how the program is designed can translate into meaningful savings for taxpayers.

A key factor in controlling costs is whether insurance premiums accurately reflect the risk of crop losses. Federal law requires premiums to be set so that they cover expected payouts over time while also helping the program prepare for unusually large disasters. To meet this goal, the Risk Management Agency regularly updates the data used to calculate premiums. These updates incorporate new information on yields, losses, and changing production conditions. Without regular updates, premiums can drift away from actual risk, potentially increasing taxpayer exposure even when subsidy rates remain unchanged.

A recently published article in Applied Economic Perspectives and Policy by an Agricultural Risk Policy Center economist examines the role of actuarial updates, which are routine adjustments to the data used to calculate insurance premiums (Tsiboe, 2026). Using data from 2002 through 2024, the study compares actual program outcomes with a hypothetical scenario in which insurance rates were not updated from one year to the next. This approach allows the researchers to estimate how much more the program would have cost if pricing had relied on outdated risk information.

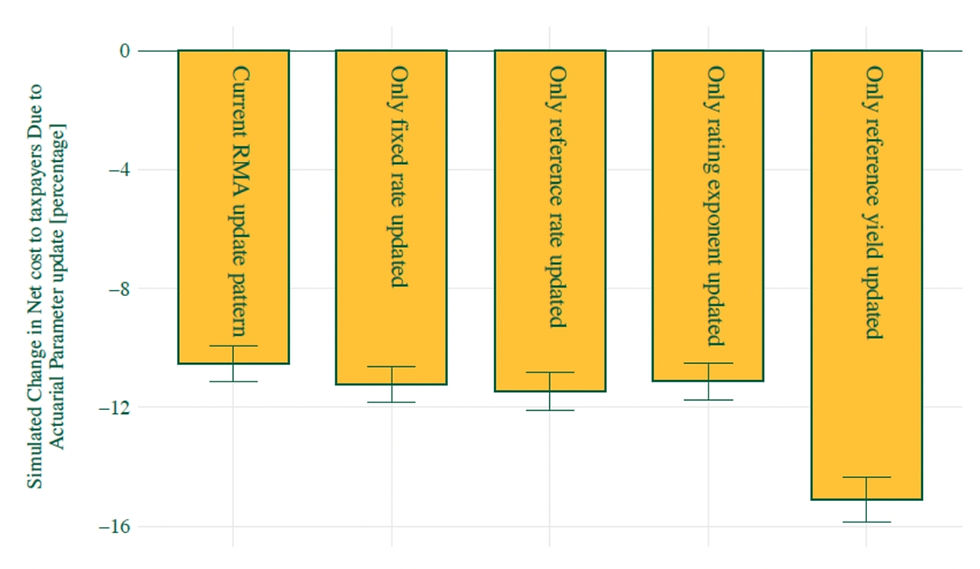

Figure 1 summarizes the estimated effects of routine actuarial updates on taxpayer outlays in the U.S. Federal Crop Insurance Program. The figure reports the simulated percentage change in taxpayer costs relative to a no update baseline under alternative actuarial update scenarios, where negative values indicate cost reductions. The bars compare the full Risk Management Agency update pattern with targeted single-parameter updates, including fixed rates, reference rates, rating exponents, and reference yields. As shown in Figure 1, routine actuarial adjustments consistently reduce taxpayer costs across all scenarios.

Under the full Risk Management Agency update pattern, government spending is reduced by about 10 percent per year on average relative to the no update case. These savings arise because updated premiums more closely reflect real-world loss risk, reducing situations in which insurance payouts exceed what premiums were designed to cover. Importantly, these reductions are achieved without cutting premium subsidies or limiting coverage, helping to preserve strong farmer participation.

The figure also shows that targeted updates, particularly to reference yields, generate even larger cost reductions, highlighting the outsized fiscal importance of specific actuarial components. By contrast, up- dating all pricing components at the same time can sometimes reduce the impact of the most influential changes, since different adjustments may move in opposite directions. This finding suggests that a more targeted and flexible update strategy could further improve fiscal efficiency.

Figure 1: Estimated Change in U.S. Federal Crop Insurance Program Taxpayer Outlays from Routine Actuarial Updates.

Note: Simulation - Actuarial Data Master [ADM] (successor) for the release year (e.g., 2023) was replaced with the ADM for the previous year (incumbent) (e.g., 2022), and the premiums were recalculated for the actual loss experience outcomes associated with the successor in the release year. Crop insurance demand at the extensive margin (insured acres) is allowed to shift based on responsiveness to paid premium rates.

Source: NDSU Agricultural Risk Policy Center (ARPC), using data from Tsiboe (2026).

As shown in Figure 2, savings from the full Risk Management Agency update pattern are not uniform across the country. States with large and stable agricultural sectors tend to see the greatest benefits, be- cause more data allows risks to be priced more accurately. States with smaller insured acreage or highly variable production conditions experience smaller gains, and in a few cases modest cost increases. These patterns highlight that agricultural risk differs widely across regions and that pricing systems perform best where information is strongest.

Figure 2: State-Level Taxpayer Cost Impacts of Actuarial Updates.

Note: Simulation - Actuarial Data Master [ADM] (successor) for the release year (e.g., 2023) was replaced with the ADM for the previous year (incumbent) (e.g., 2022), and the premiums were recalculated for the actual loss experience outcomes associated with the successor in the release year. Crop insurance demand at the extensive margin (insured acres) is allowed to shift based on responsiveness to paid premium rates.

Source: NDSU Agricultural Risk Policy Center (ARPC), using data from Tsiboe (2026).

The study also emphasizes important tradeoffs. More frequent or more targeted updates can increase year to year changes in premiums, which may affect how farmers perceive program stability. Existing safe- guards, such as limits on annual rate changes and smoothing methods, help reduce sharp swings, but clear communication remains essential. Farmers are more likely to trust the program when they understand why prices change and how updates improve long-term stability.

Overall, the findings indicate that improvements in how crop insurance risk is measured and priced are closely associated with lower taxpayer costs. The analysis suggests that actuarial updates can influence program expenditure without necessarily reducing premium subsidies or coverage levels, which are important for maintaining participation. As a cornerstone of U.S. agricultural policy, the U.S. Federal Crop Insurance Program operates through a public-private partnership that supports farmers, sustains domestic food production, and contributes to broader economic stability. With taxpayer support averaging about $2.18 per month per American since 2008, efficient use of public funds remains an important consideration. The results show that targeted, adaptive actuarial updates are linked to reductions in taxpayer liabilities, improved fiscal discipline, and continued provision of risk protection for producers. Taken together, the evidence points to the role of pricing accuracy, rather than reduced protection, in shaping the fiscal sustainability of the crop insurance system while preserving a secure food supply.

References

Tsiboe, Francis (2026). Routine Actuarial Adjustments Cut Taxpayer Cost in Subsidized Agricultural Insurance. Applied Economic Perspectives and Policy. Online Version of Record before inclusion in an issue. https://doi.org/10.1002/aepp.70052.

Comments